Debt piling up? See how the “50/30/20 Budget” can save your savings and freedom in one year! and freedom in one year!

Sarah sat at her kitchen table in Austin, staring at a stack of overdue notices. The weight of her debt felt like a heavy burden she carried every single day. She tried various mobile apps, but none seemed to work with her lifestyle.

Everything changed when she adopted a straightforward approach to her cash flow. This system does not require complex mathematics or restrictive lifestyle modifications that are difficult to maintain. It provides a clear lens through which you can evaluate every dollar you earn.

She used the 50/30/20 Budget to stop the cycle of debt for good. You can reach your goals with financial freedom planning in just one year. This Method transforms your relationship with your earnings and creates a path toward lasting security.

This guide provides the essential tools to reclaim control of your future. You will learn to balance immediate requirements with significant long-term objectives. Soon, you will feel empowered to manage your personal assets with absolute confidence.

Key Takeaways

- Master the basics of financial planning to organize your monthly bills.

- Create a sustainable reserve habit to protect against unexpected expenses.

- Balance your essential needs and personal wants without feeling guilty.

- Reduce high-interest debt with a proven, systematic framework.

- Achieve total control over your cash flow to ensure long-term growth.

What Is the 50/30/20 Budget and Why It Works for Debt Elimination

If you’ve ever felt lost in complex spreadsheets, the 50/30/20 Budget is a breath of fresh air. It became famous thanks to Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi. They shared this simple way to manage money in their book, All Your Worth: The Ultimate Lifetime Money Plan.

This Method has stood the test of time because it focuses on big numbers rather than tiny details. It’s a break from the endless tracking of every penny. It helps you live well today while planning for tomorrow.

The Simple Framework That Makes Budgeting Actually Work

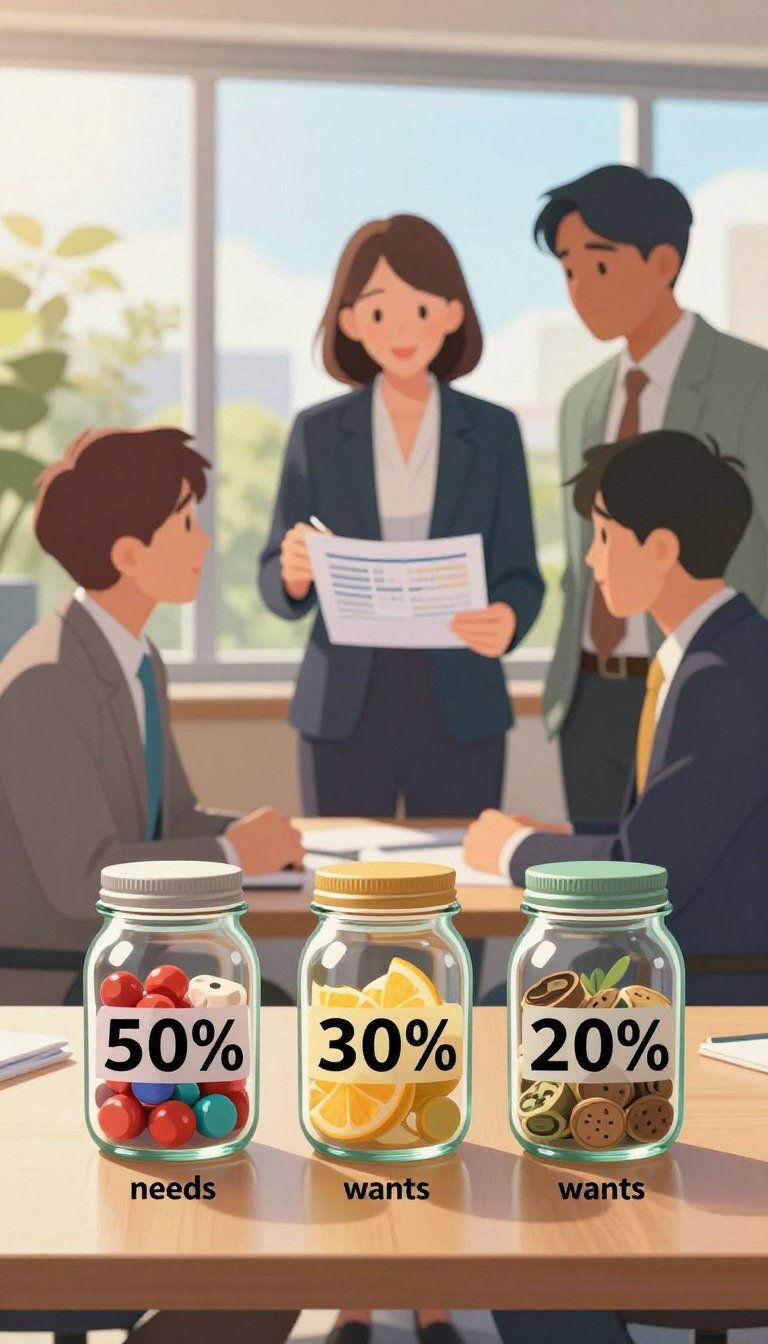

The core idea is to split your after-tax income into three parts. You spend 50% on needs, 30% on wants, and 20% on savings and debt. This makes budgeting easy without constant stress.

Using these broad categories, you feel in control of your money. No more worrying if a coffee will break your Budget. Just keep your “wants” under 30% to keep your 50/30/20 Budget in check.

This approach is why many stick to it long-term. It avoids the deprivation of strict budgets. You can enjoy life while knowing your basics are covered.

| Category | Allocation | Common Examples |

|---|---|---|

| Needs | 50% | Rent, Utilities, Groceries, Insurance |

| Wants | 30% | Dining out, Hobbies, Subscriptions |

| Savings & Debt | 20% | Credit card payments, Emergency fund |

Why Financial Experts Recommend This Method for Debt Freedom

Certified financial planners often recommend this Method. It tackles the emotional side of money. Extreme limits can lead to frugal fatigue, causing people to quit. The 50/30/20 Budget keeps your life enjoyable while you work towards debt freedom.

This approach is flexible, making it the best budgeting advice for changing lives. It fits different incomes and keeps debt repayment a priority. You can adjust it as your life changes without starting over.

“A budget is telling your money where to go instead of wondering where it went.”

Studies show balanced methods work better than extreme ones. Seeing your savings grow while enjoying life keeps you on track. This mental boost is the best budgeting advice for beating debt for good.

Understanding the Three Categories of the 50/30/20 Budget Rule

Success with the 50/30/20 rule comes from knowing the difference between needs and wants. It divides your after-tax income into three parts. This helps you cover your basics and work towards your goals.

Many people struggle with debt because they don’t have a clear spending plan. This rule makes it easier to choose how to spend your money. It helps you find a balance that lets you enjoy life while saving for the future.

50% for Needs: Your Non-Negotiable Essential Expenses

Your “needs” are what you must pay for to stay healthy, safe, and employed. This includes rent, mortgage, property taxes, and insurance. You also need to pay for utilities, basic groceries, and healthcare.

Remember, paying the minimum on debts is also a need. While you want to pay off debt fast, you must keep up with the minimum payments. This rule shows why your needs should not take up more than half of your income.

If your needs exceed 50%, you might have too much debt. High costs leave little room for savings or emergencies. You might need to rethink your lifestyle if your essentials take up most of your income.

“A budget is telling your money where to go instead of wondering where it went.”

30% for Wants: Maintaining Balance While Getting Out of Debt

The “wants” category can be tricky for those looking for budgeting advice. These are things that make life better but aren’t essential. Examples include dining out, streaming services, hobbies, and internet upgrades.

It might seem hard to spend 30% on fun while paying off debt. But not spending at all can lead to overspending. Setting aside money for fun makes your Budget more manageable.

Spending wisely on wants can actually help you pay off debt faster. Enjoying a coffee or a movie night is okay if it’s within your Budget. This balance keeps you motivated to reach your financial goals.

20% for Savings and Debt Repayment: Building Your Financial Future

This 20% is key to growing your wealth and paying off debt. First, build an emergency fund of $1,000 to $2,000. This fund helps you avoid using credit cards for unexpected expenses.

Once you have your emergency fund, focus on paying off debt aggressively. Use budgeting advice to decide which debts to tackle first. This shows your commitment to your financial future and independence.

| Category | Percentage | Key Examples |

|---|---|---|

| Needs | 50% | Rent, Utilities, Minimum Debt |

| Wants | 30% | Dining Out, Travel, Hobbies |

| Savings/Debt | 20% | Extra Debt Payoff, Emergency Fund |

As you pay off debt, your 20% will go towards saving for retirement and building wealth. The 50/30/20 rule is flexible and helps you design a life of freedom.

Step-by-Step Guide to Implementing Your 50/30/20 Budget This Month

Starting to manage your money means having a clear plan. You need more than just ideas to see real changes in your bank account. These money management techniques offer a step-by-step guide to help you control your income. By following these steps, you can move from financial uncertainty to full control in just four weeks.

Many people struggle with budgeting because they try to do too much at once. This guide breaks it down into easy steps that anyone can follow. You’ll learn to look at your money objectively and make choices that support your long-term goals. Let’s start your personal finance tips journey.

Step 1: Calculate Your True After-Tax Monthly Income

Your Budget needs to be based on the money you actually get. Many people use their gross salary, but this leads to overspending. You should use your net pay, which is your take-home pay after taxes and other deductions.

If you have a steady salary, look at your latest pay stubs. Multiply your weekly pay by 52 and divide by 12, or your bi-weekly pay by 26 and divide by 12. This gives you a consistent monthly amount for your Budget.

For those with variable income, like freelancers or hourly workers, use a conservative average. Look at your earnings from the last three to six months and pick the lowest or average amount. Include side hustles and bonuses only if they are regular and reliable.

Step 2: Track Every Dollar You Spend for 30 Days

You can’t manage what you don’t measure. Before you can assign money to categories, you must know where it goes. Commit to tracking every single purchase for at least 30 days to build a data foundation.

Choose a method that feels natural to you. You might prefer a smartphone app that syncs with your bank, or a simple notebook you carry in your pocket. The goal is to capture all purchases, big and small.

Don’t judge your spending during this phase. Just record the facts so you have an honest picture of your habits. This transparency is key for the next steps.

Step 3: Categorize Your Expenses Honestly

After 30 days of data, sort your spending into the three 50/30/20 buckets. This requires honesty about what is a “need” versus a “want.” You might find some expenses are in a gray area.

A “need” is something required for survival or for maintaining your employment, such as rent or basic groceries. A “want” is anything that improves your quality of life but is not strictly necessary. Be strict with yourself during this process to ensure your Budget remains realistic.

For example, high-speed internet might be a need if you work from home. But the top-tier streaming package attached to it is definitely a want. Separate these costs to see the truth of your spending.

Step 4: Identify Gaps and Make Necessary Adjustments

Now, compare your current spending percentages to the 50/30/20 targets. Most people find they spend more than 30% on wants or more than 50% on needs. These personal finance tips help you bridge that gap effectively.

If your needs exceed 50%, look for ways to reduce fixed costs, such as insurance or utilities. If your wants are too high, identify the “low-hanging fruit,” such as unused subscriptions. Small adjustments in several areas often add up to significant monthly savings.

Step 5: Automate Your Savings and Debt Payments

Willpower is a limited resource that often fails when we are tired or stressed. Automation removes the need for daily discipline by handling the heavy lifting for you. Set up automatic transfers to your savings and debt accounts on the day you get paid.

Treat your 20% savings and debt goal like a bill that you must pay. When the money leaves your account immediately, you learn to live on the remaining 80%. This “pay yourself first” mentality is the secret to long-term wealth building.

Step 6: Create Your Personalized Spending Plan

The final step is to turn your data into a forward-looking plan. Use your money management techniques to set weekly spending limits for your “wants” category. This prevents you from running out of money before the month ends.

Review your plan every Sunday to see how you performed the previous week. Adjust your spending for the coming days based on what is left in your Budget. This simple habit keeps you focused and ensures you hit your 50/30/20 targets every single month.

| Implementation Phase | Critical Task | Primary Tool | Success Metric |

|---|---|---|---|

| Income Audit | Verify net take-home pay | Pay stubs / Bank statements | Accurate monthly baseline |

| Data Collection | Log all transactions | Tracking app or notebook | 30 days of complete data |

| Gap Analysis | Compare actuals to targets | 50/30/20 Calculator | Identified areas for cuts |

| System Setup | Automate transfers | Online banking portal | Zero-effort debt payments |

| Maintenance | Weekly budget review | Personal spending plan | Staying within category limits |

Money Saving Tips to Shrink Your Needs Category Below 50%

Lowering your essential spending to under 50% is key to paying off debt. The 50/30/20 rule is a good starting point. But treat it as a maximum, not a goal. This way, you can save more and pay off debt faster.

Using money-saving tips helps you manage your money more effectively. Cutting down on rent or groceries means more money for your future. These personal finance tips lead to big savings without needing constant effort.

“The fastest way to increase your wealth is to lower your cost of living without lowering your quality of life.”

Reduce Housing Costs Without Sacrificing Comfort

Housing costs are usually the biggest part of your expenses. Look into sharing your home with a roommate. If you own your home, refinancing can save you thousands over time.

Consider house hacking by renting out a spare room. You might also challenge your property tax if you think your home is overvalued. If you rent, try to get a lower rent by taking care of small repairs or signing a longer lease.

Cut Transportation Expenses by 20% or More.

Transportation costs are often second only to housing. Calculate your cost per mile to understand your expenses better. If your car payment is too high, consider selling your car and using public transit.

Carpooling or working from home can save you a lot on fuel and maintenance. Doing simple car maintenance yourself can also save money. Always use apps to find the cheapest gas prices.

Lower Your Insurance and Utility Bills Through Negotiation

Many people pay too much for insurance by not shopping around. Shop your auto and home insurance every year to find better deals. Bundling policies and raising deductibles can also lower your premiums.

For utilities, negotiation is your best friend. Use scripts to negotiate better rates with your internet or cell phone provider. Installing a smart thermostat and sealing air leaks can also cut your energy bills by 10% to 15% each month.

Smart Grocery Shopping Strategies That Save Hundreds Monthly

Groceries are a flexible area where you can see quick results from money-saving tips. Plan your meals to avoid buying too much. Buying store brands instead of name brands can save you a lot of money.

Focus on seasonal produce and buy non-perishable items in bulk. Use loyalty programs and cash-back apps to earn rewards. Reducing Food waste means your money doesn’t go to waste.

| Expense Category | Optimization Strategy | Estimated Monthly Savings | Difficulty Level |

|---|---|---|---|

| Housing | Refinancing or House Hacking | $200 – $600 | High |

| Transportation | Carpooling & DIY Maintenance | $50 – $150 | Medium |

| Utilities | Provider Negotiation | $30 – $80 | Low |

| Groceries | Meal Planning & Store Brands | $100 – $300 | Medium |

How to Optimize Your 30% Wants Without Feeling Deprived

Mastering the 50/30/20 rule is all about managing your 30% for personal desires. It’s easy to cut this category when debt mounts, but total deprivation is a recipe for failure. With the right budgeting advice, you can enjoy life’s luxuries while keeping your financial goals in sight.

Change your mindset to see the abundance of options rather than what you’re missing. You can indulge in modern comforts and social activities without emptying your wallet every weekend. These money-saving tips help keep your lifestyle both enjoyable and sustainable as you work towards financial freedom.

Finding Free and Low-Cost Entertainment Alternatives

Your local community is a treasure trove of free entertainment. Many overlook the public library, which offers more than just books. Libraries now provide free museum passes, digital streaming, and even special equipment for hobbies.

Outdoor activities are another great way to stay active and connected without spending money. Explore state parks, join community sports, or attend free festivals. These activities bring genuine satisfaction and social connections without the high cost of ticketed events.

Here are some weekly planning comparisons:

| Activity Category | High-Cost Choice | Low-Cost Alternative | Potential Savings |

|---|---|---|---|

| Movie Night | Premium Cinema | Library Streaming | $40.00 |

| Fitness | Boutique Studio | Community Yoga | $25.00 |

| Learning | Paid Workshop | Free Online Course | $100.00 |

The Strategic Approach to Dining Out and Subscriptions

American households often waste money on unused digital subscriptions. Monthly audits can help you identify unused services. Switching streaming services instead of paying for all at once can save hundreds a year.

When it comes to dining out, budgeting advice can make a big difference. Opt for happy hour or brunch instead of expensive dinners. Lunch menus often offer the same quality at a lower cost.

“A budget is telling your money where to go instead of wondering where it went.”

Rewarding Yourself While Staying on Track

Psychological rewards are key to sticking to your financial plan. Include “proportional rewards” in your schedule to celebrate milestones. These small treats acknowledge your efforts without jeopardizing your debt repayment.

- Celebrate a $1,000 debt reduction with a special home-cooked meal.

- Enjoy a “guilt-free” coffee at your favorite shop after a successful month.

- Use a small part of your 30% for a book or a hobby tool.

By rewarding yourself wisely, you reinforce good financial habits. This approach makes you feel empowered within your 50/30/20 Budget. Small victories add up to big successes over time.

Maximizing Your 20% for Aggressive Debt Payoff and Wealth Building

Your journey to lasting wealth starts with how you use the 20% of your income for savings and debt. This 20% is key to your financial growth. The other 80% covers your daily life, but this 20% secures your financial future.

It’s important to handle this 20% with absolute discipline. It’s not for spending when you have a good month. It’s for breaking the cycle of living paycheck to paycheck.

Splitting Your 20% Between Emergency Fund and Debt Repayment

Deciding where to send your money first is a big challenge. You might want to pay off your credit cards right away. But, without a safety net, a small problem could lead to more debt.

Most experts suggest a phased approach. Start with a starter emergency fund of $1,000 to $2,000. This small fund protects your Budget from small surprises while you focus on your main goals.

- Phase 1: Put your full 20% into your starter emergency fund until you reach your goal.

- Phase 2: Move that 20% to your high-interest debt until it’s gone.

- Phase 3: Grow your emergency fund to cover three to six months of living expenses. Split this amount based on your life situation. If your job or health is unstable, build a bigger initial cushion. Always prioritize your financial stability before aggressively paying off debt.

Choosing the Right Debt Payoff Strategy for Your Situation

Once your starter fund is ready, you need a plan to tackle your debt. The Debt Snowball and the Debt Avalanche are the main methods. Choose based on whether you value quick wins or saving money on Interest.

| Strategy | Primary Focus | Main Benefit |

|---|---|---|

| Debt Snowball | Smallest Balance First | Quick Psychological Wins |

| Debt Avalanche | Highest Interest Rate First | Saves Most Interest Money |

| Hybrid Method | High Interest then Small Balance | Balanced Motivation |

The Debt Avalanche is the most efficient way to save on Interest. Pay the highest interest rate first. This Method saves you the most money over time.

The Debt Snowball focuses on human behavior. Pay off the smallest balance first for quick wins. This builds momentum for long-term financial freedom planning.

When to Start Investing While Still Carrying Debt

Should you wait to invest until you’re debt-free? Often, waiting can cost you thousands. The key is to look at your current interest rates.

If your employer matches your 401(k), contribute enough to get the full match. This is a 100% return on your money. No debt interest rate can beat that.

“Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.”

For other investments, use the 4%-5% rule. If your interest rate on debt is higher than 5%, pay it off first. If it’s lower, like a mortgage, invest instead.

Using Extra Income to Accelerate Your Financial Freedom Timeline

While the 50/30/20 Budget is good, you can reach your goals faster with more 20%. You don’t always need to cut more “wants” to find extra money. Sometimes, the best way is to increase your total income.

Use windfalls like tax refunds or bonuses to make big debt payments. These one-time payments can cut months or years off your repayment time. They are a powerful boost for your financial freedom planning.

- Side Hustles: Use skills like writing, driving, or consulting to earn extra cash.

- Salary Negotiation: Research market rates and ask for a raise at your current job.

- Selling Items: Clear out your home and sell unused electronics or furniture online.

Every extra dollar should go into your 20% category. By keeping your lifestyle the same while your income grows, you create a huge surplus. This surplus is the key to achieving financial independence quickly.

Common Budgeting Mistakes That Derail Your 50/30/20 Success

Many people struggle with budgeting, not because they lack discipline. It’s often because they fall into common traps. Even with a good plan, small mistakes can lead to big financial problems. Knowing these pitfalls is key to achieving financial freedom.

By following expert budgeting advice, you can avoid these common mistakes. Most failures occur when the plan looks good on paper but doesn’t match real life. Let’s explore the most common mistakes that might be holding you back.

The Trap of Miscategorizing Wants as Needs

One common error is calling a “want” a “need.” For example, you might think you need a $1,200 smartphone for work. But a mid-range model can do the job just as well.

This kind of thinking can make your “needs” category too big. If it takes up 60% or 70% of your income, paying off debt becomes hard. You need to be honest about where your money goes each month.

To fix this, use the “Job Loss Test.” Ask yourself: “Would I keep paying for this if I lost my job tomorrow?” If no, it’s a want, not a need. This simple question helps you apply professional budgeting advice to your spending.

Failing to Account for Irregular and Annual Expenses

Many budgets work well for 10 months but fail when “surprise” bills come in. Costs like car registration and property taxes are predictable. Yet, many forget to include them in their monthly Budget.

Effective money management techniques involve a “sinking fund” for these costs. List all non-monthly expenses, like holiday gifts and back-to-school shopping. Divide the total by 12 to find your monthly amount.

See this monthly amount as a non-negotiable bill. Saving a bit each month avoids the stress of big bills. This keeps your 50/30/20 plan stable all year.

Setting Unrealistic Expectations and Burning Out

It’s tempting to try a strict 40/20/40 split to get out of debt fast. But if you’re currently spending 70/25/5, a big change like that usually fails. Trying too hard can lead to decision fatigue and burnout.

A budget is not just about numbers; it is about managing your behavior over a long period of time.

The best budgeting advice is to make small, incremental changes. Start by making your budget 10% to 15% more restrictive than your current spending. Once you maintain that for three months, you can tighten it further without feeling deprived.

Not Adjusting Your Budget as Your Income Changes

Your Budget should grow with your career. Many people spend more as their income rises. This keeps them financially stuck, no matter how much they earn.

Advanced money management techniques suggest keeping your spending the same after a raise. Instead of buying a pricier car, use the raise to pay off debt. This speeds up your path to financial freedom.

Review your 50/30/20 percentages whenever your income changes by more than 5%. This keeps your spending in line with your wealth-building goals. Consistency, not perfection, is key to managing your money well.

| Mistake Type | Common Example | The Solution |

|---|---|---|

| Miscategorizing | High-end gym memberships | Use the “Job Loss Test” |

| Irregular Costs | Annual car insurance | Create a monthly sinking fund |

| Burnout | Cutting all fun spending | Use 10-15% incremental shifts |

| Income Shifts | Buying a newer car after a raise | Redirect raises to debt payoff |

Essential Tools and Apps for Tracking Your 50/30/20 Budget

Finding the right app or spreadsheet can make budgeting fun. The 50/30/20 rule is easy, but tracking every transaction needs the right system. These personal finance tips will help you choose a tool that suits your skills and lifestyle.

The right tool is like a financial GPS. It shows you where your money is at any time. Whether you like automated syncs or manual entry, there’s a tool for you.

Using these tools well means you’ll never wonder where your money went. You can focus on your goals without getting lost in numbers. Here’s the best budgeting advice for choosing your tracking platform.

Top Budgeting Apps That Automate the 50/30/20 Method

Modern apps make it easy to categorize spending into needs, wants, and savings. YNAB (You Need A Budget) uses zero-based budgeting. It’s easy to adjust its categories to fit the 50/30/20 rule.

EveryDollar is great for beginners with its simple interface. It lets you quickly move transactions into categories. It shows you how much you have left to spend each month.

PocketGuard clearly shows your “spendable” money. It calculates bills and savings goals first. This stops you from spending “needs” money on “wants”.

Goodbudget offers a digital version of the envelope method. It’s perfect for couples because you can share your Budget. It turns your 50%, 30%, and 20% into virtual envelopes.

Simple Spreadsheet Templates for Manual Tracking

Some people like the control that a manual spreadsheet offers. Google Sheets or Microsoft Excel lets you customize every row. You can create a template that automatically calculates percentages using simple formulas.

Manual tracking is a great personal finance tip for awareness. When you enter every coffee or grocery bill, you see the impact. This hands-on experience often leads to better spending habits.

You can use conditional formatting to highlight overspending. Many free templates online are already set up for the 50/30/20 rule.

How to Conduct Effective Weekly Budget Reviews

A tool is only useful if you check it regularly. Make a 15-minute weekly review a habit. Sunday mornings are a good time to review your finances.

During your review, check any uncategorized transactions. See if you’re close to your “wants” limit for the month. This lets you make small changes before overspending.

Use this time to celebrate small victories, like staying under Budget. Regular budgeting advice says check-ins prevent big surprises. It turns budgeting into manageable weekly tasks.

| Tool Name | Best Feature | Tracking Style | Target User |

|---|---|---|---|

| YNAB | Zero-based planning | Automated/Proactive | Detailed Planners |

| EveryDollar | Simple interface | Manual or Auto | Budgeting Beginners |

| PocketGuard | “In My Pocket” view | Automated | Overspenders |

| Google Sheets | Total customization | Manual | Privacy Seekers |

| Goodbudget | Digital envelopes | Manual entry | Visual Spenders |

What Financial Freedom Looks Like After One Year on the 50/30/20 Budget

After a year on the 50/30/20 Budget, your finances have changed a lot. You’ve moved from worrying about money to having control over it. This change isn’t just about money; it’s about the peace of mind you’ve gained through discipline.

Starting with financial freedom planning means seeing these real results. By following the 50/30/20 rule, you’ve built a strong base for long-term stability. Let’s look at the milestones you can hit after 365 days of commitment.

Realistic Debt Reduction Milestones to Expect

Your progress is based on your income, but the 50/30/20 rule helps everyone. If you make $50,000 a year, you have about $3,200 a month after taxes. Putting 20% of that toward debt means you pay $640 each month.

In a year, that’s $7,680 toward your debt. If you focus on high-interest credit cards, you can clear $8,000 to $9,000 of debt. Seeing your debt go down to zero boosts your motivation.

Building Your Emergency Fund from Zero to Three Months

For the first six months, split your 20% between savings and debt. This means $320 per person, for a total of $1,920 in an emergency fund. This small fund helps you avoid using credit cards for unexpected expenses.

Once you have $2,000 saved, you can focus more on paying off debt. This balanced approach helps you avoid old spending habits. It gives you the confidence to stay on track, even when life gets unpredictable.

Improved Credit Score and Financial Confidence

Being consistent with your payments improves your credit score as much as your savings. By paying on time and lowering your credit use, your score can rise by 50 to 100 points in a year.

But it’s not just about the numbers. You’ll also feel more confident about your finances. You won’t dread checking your bank app or getting mail from lenders. This confidence lets you make financial choices based on your goals, not fears.

Transitioning from Debt Payoff to Wealth Building

Once your high-interest debts are gone, you start the exciting part of financial freedom planning. The 20% you used to pay creditors is now yours. You can explore investing strategies to grow your money.

You might put this money into a 401(k), a Roth IRA, or a brokerage account. The habits you built while paying off debt are perfect for building wealth. You’re not just surviving; you’re creating a financial legacy.

| Monthly Net Income | Annual Debt Payoff (20%) | EmergSplitFund (6-Mo Split) | Focus for Year Two |

|---|---|---|---|

| $3,000 | $7,200 | $1,800 | Investing strategies |

| $4,500 | $10,800 | $2,700 | Retirement growth |

| $6,000 | $14,400 | $3,600 | Wealth accumulation |

Conclusion

Starting to control your money begins with a clear plan. The 50/30/20 Budget is a simple way to balance your life and finances. It divides your income into three parts: needs, wants, and savings.

This Method is effective because it doesn’t ask for too much sacrifice. You can live well while saving for the future.

Your journey to financial freedom starts with tracking your first dollar. Use tools like Rocket Money or YNAB to see where your money goes. Making small changes can lead to big results over the course of a year.

You can pay off credit card debt at Chase or Wells Fargo. You can also build a solid emergency fund at Ally Bank.

Begin by finding your after-tax monthly income. Look at your pay stubs from the last month. List your fixed costs, such as rent and utilities.

Consistency is more important than getting every penny right at first. You have the power to change your financial story right now.

Effective financial planning turns stress into security. Stick to the 50/30/20 Budget and watch your savings grow. You have the tools and roadmap to succeed.

Your future self will thank you for the steps you take today.